Buying or selling a home is exhilarating. However, home insurance issues before closing in Eagle Idaho can abruptly stall the momentum. Lenders require proof of homeowners insurance before funding a loan. Therefore, even a minor underwriting snag can jeopardize your timeline.

In today’s evolving insurance climate, especially across Boise Idaho, underwriting scrutiny has intensified. Consequently, buyers and sellers in Eagle Idaho must be proactive rather than reactive. As a top realtor in Eagle, Chris Budka ensures clients understand how insurance complications can impact contracts, appraisals, and ultimately, closing day.

Let’s unpack what really happens when insurance becomes an issue before closing—and how to navigate it with confidence.

Why Homeowners Insurance Is Required Before Closing

Mortgage lenders mandate insurance coverage because they have a vested financial interest in the property. In fact, until the loan is paid off, the lender technically holds an interest in the asset.

According to the National Association of Realtors, proof of insurance is a non-negotiable closing condition for financed purchases. Without it, lenders will not release funds. Therefore, if a policy cannot be secured, closing cannot occur.

This is particularly relevant in Eagle Idaho real estate markets where higher-value homes may require specialty coverage. Additionally, properties near foothills or open land may trigger wildfire risk assessments. As a result, underwriters may require inspections or deny coverage outright.

Common Home Insurance Issues Before Closing in Eagle Idaho

Insurance hurdles are more common than most buyers expect. However, understanding them in advance can prevent last-minute stress.

1. Roof Condition Concerns

Insurers often request the age of the roof. If it is nearing the end of its lifespan, coverage may be limited or denied. Meanwhile, lenders will not approve a loan without adequate protection.

Older homes in established Eagle Idaho neighborhoods sometimes face this scrutiny. Consequently, sellers may need to replace or certify the roof before closing.

2. Claims History on the Property

Insurance companies review the property’s claims history through the CLUE database. If multiple prior claims exist, premiums may spike or coverage may be denied.

This can surprise buyers exploring homes for sale in Eagle Idaho, especially when the property appears well maintained. Therefore, reviewing disclosures carefully is essential.

3. Wildfire Risk Assessments

With Idaho’s dry summers, some carriers evaluate wildfire exposure. According to Idaho.gov, wildfire mitigation has become a statewide focus.

Properties bordering open land in Eagle ID may require additional underwriting. In some cases, insurers request defensible space improvements before issuing a policy.

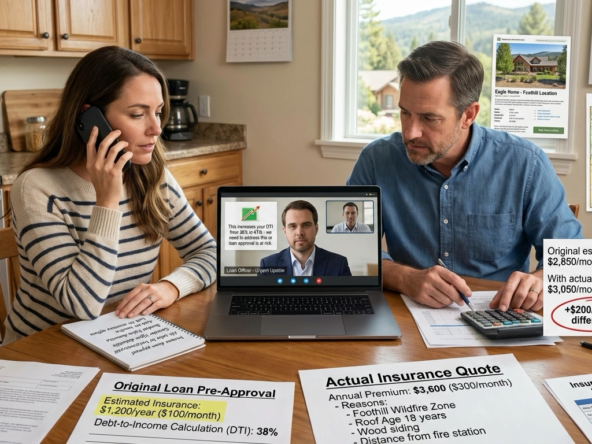

4. High Replacement Cost Estimates

Luxury Eagle ID homes often have elevated rebuild costs. Consequently, insurance premiums may exceed initial buyer estimates. If coverage strains debt-to-income ratios, loan approval may be impacted.

What Happens to Your Closing Timeline?

Insurance delays can trigger several cascading effects.

First, lenders cannot issue final approval without an insurance binder. Therefore, your closing date may need to be extended.

Second, rate locks may expire. Additionally, moving schedules may require adjustment. For families relocating and moving to Idaho, this can create logistical challenges.

According to the U.S. Census Bureau, Idaho continues to experience strong inbound migration. Meanwhile, increased demand can tighten insurance carrier capacity. As a result, starting insurance quotes early is prudent.

An experienced Eagle ID realtor anticipates these variables and builds contingency plans into the contract.

Can a Deal Fall Apart Over Insurance?

Yes. However, it is uncommon when guided properly.

If a buyer cannot obtain insurance at reasonable rates, the financing contingency may allow contract termination. Therefore, proactive communication is critical.

Sellers also face risk. For instance, if a roof or structural issue is flagged during underwriting, repairs may become necessary to preserve the transaction.

As the best realtor in Eagle ID, Chris Budka coordinates between lenders, insurance agents, and inspectors. Consequently, small problems rarely escalate into failed closings.

Solutions When Insurance Becomes an Issue Before Closing

The good news? Most home insurance issues before closing in Eagle Idaho are solvable.

Shop Multiple Carriers

Insurance underwriting varies by provider. Therefore, if one carrier declines coverage, another may approve it.

Buyers purchasing Eagle ID homes for sale should consult independent insurance brokers early in escrow.

Complete Required Repairs

If an insurer requires minor corrections—such as installing handrails or replacing a section of roof—addressing them quickly can restore eligibility.

Adjust Coverage Structure

Sometimes increasing deductibles or modifying optional endorsements can make premiums workable. Meanwhile, lenders simply require minimum hazard coverage to fund the loan.

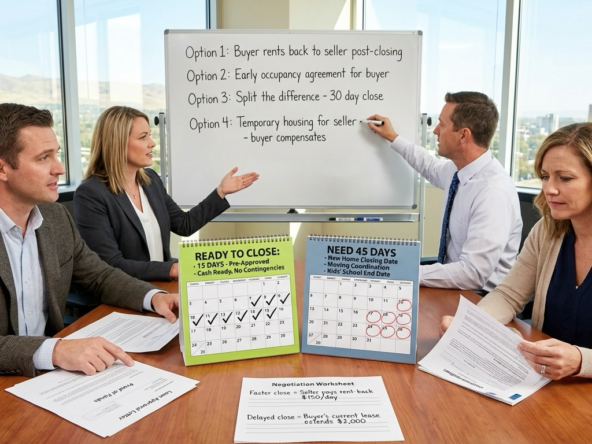

Request a Closing Extension

If insurance approval is pending, negotiating a short extension can preserve the deal. In Eagle Idaho real estate transactions, communication and documentation are essential.

How Sellers Can Prevent Insurance Delays

Preparation mitigates surprises.

Before listing, consider a pre-listing inspection. Additionally, confirm roof age and HVAC condition. These steps can protect your timeline.

If you’re planning to sell your home, a preemptive strategy ensures buyers won’t encounter last-minute underwriting refusals.

Sellers who obtain a market analysis before listing also position themselves strategically. Pricing correctly reduces prolonged exposure, which can sometimes complicate insurance renewals.

Why Insurance Issues Are Increasing in Idaho

Several macroeconomic factors contribute.

Construction costs have risen. Consequently, replacement values are higher. According to Realtor.com, rebuilding expenses nationwide have climbed due to labor and material volatility.

Additionally, climate modeling has shifted underwriting guidelines. As more Americans move to Idaho, housing density changes risk modeling patterns.

However, Eagle Idaho remains one of the most desirable communities in the Treasure Valley. With strong schools, refined amenities, and proximity to Boise Idaho, buyer demand continues to thrive.

The Role of a Skilled Eagle Idaho Realtor

Insurance complications require coordination. Therefore, working with an experienced Eagle Idaho realtor becomes invaluable.

Chris Budka of Chris Budka Real Estate proactively discusses insurance during the offer stage. Meanwhile, timelines are structured to allow underwriting clearance.

Buyers benefit from local insight into the best neighborhood in Eagle. Sellers gain strategic preparation that limits underwriting objections.

Whether purchasing Eagle Idaho homes for sale or preparing to sell, expert representation shields your equity and timeline.

How to Avoid Home Insurance Issues Before Closing in Eagle Idaho

Prevention is preferable to remediation.

First, request insurance quotes immediately after going under contract. Additionally, provide full property disclosures to your agent and insurer.

Second, review the Comprehensive Loss Underwriting Exchange (CLUE) report when possible.

Third, consult local professionals who understand Eagle Idaho neighborhoods and insurance nuances.

Ultimately, preparation transforms potential obstacles into manageable steps.

Insurance and Luxury Homes in Eagle ID

Higher-end properties demand specialized policies. For example, custom finishes, expansive square footage, and detached structures require nuanced coverage.

Consequently, buyers of luxury Eagle ID homes should engage carriers experienced in high-value policies. Meanwhile, underwriting inspections may be more detailed.

Nevertheless, the prestige and lifestyle benefits of Eagle Idaho far outweigh temporary insurance logistics.

Insurance Issues and Relocating Families

Families moving to Idaho from other states often underestimate regional underwriting criteria. However, climate, construction types, and replacement costs differ from coastal markets.

Relocation clients working with a top realtor in Eagle benefit from early insurance guidance. Additionally, coordination with local lenders ensures smoother underwriting.

FAQs

What if my insurance company denies coverage before closing?

If coverage is denied, you must seek alternative carriers immediately. Meanwhile, your lender cannot fund the loan without proof of insurance. Acting quickly typically resolves the issue.

Can a seller refuse to make insurance-related repairs?

Yes, sellers can refuse. However, doing so may jeopardize the transaction. Therefore, negotiation and strategic compromise are often necessary.

How early should I shop for insurance?

Ideally, begin immediately after your offer is accepted. Consequently, you allow time to resolve underwriting concerns without delaying closing.

Do insurance issues affect cash buyers?

Cash buyers are not required by lenders to carry insurance before closing. However, obtaining coverage remains strongly advisable.

How can Chris Budka help prevent closing delays?

Chris coordinates with lenders, inspectors, and insurance agents from day one. Therefore, potential issues are identified early, reducing surprises.

Bottomline

Home insurance issues before closing in Eagle Idaho can feel disruptive. However, they are rarely insurmountable. With strategic planning, responsive communication, and expert guidance, transactions stay intact.

Eagle Idaho continues to attract discerning buyers seeking lifestyle, stability, and long-term value. Whether buying or selling, working with a trusted professional safeguards your investment.

If you’re navigating Eagle Idaho real estate and want clarity at every step, connect with Chris Budka. Preparation today ensures a seamless closing tomorrow.